FY2025 Financial Statement Filing Deadlines in Thailand — And Who Must Sign

A complete guide to Thailand's FY2025 financial statement filing deadlines (AGM, DBD, PND.50) plus the three signatures every set of accounts needs — director, registered accountant, and CPA auditor. Cites CCC §1197, Accounting Act B.E. 2543, and the Revenue Code.

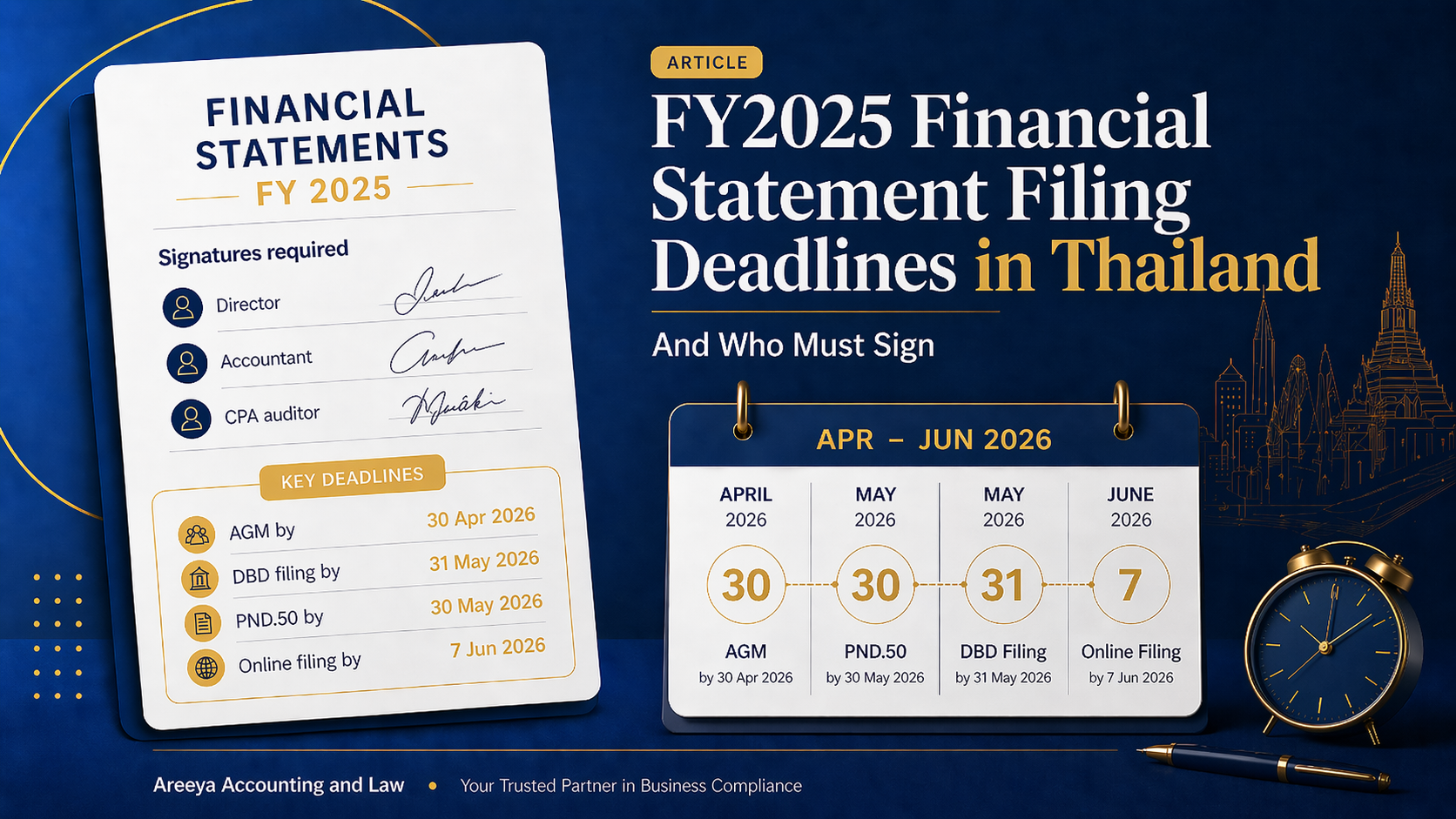

If your company runs on a calendar year like most, 31 December year-end kicks off the busiest season — closing the books, getting them audited, filing with DBD, and filing the tax return. A lot of business owners aren’t sure what’s due when, who has to sign the accounts, and what happens if a deadline slips. Here’s the complete picture, with every legal reference you need.

Four deadlines you can’t miss

For a company with a 31 December 2025 year-end, these four dates fall between April and June 2026:

1. Hold the Annual General Meeting (AGM) — no later than 30 April 2026

The law gives you 4 months after year-end to bring shareholders together and have them approve the audited accounts — not a draft. The audit has to be finished first.

Legal basis: CCC §1197

2. File the shareholder list (Bor.Or.Jor.5) with DBD — within 14 days of the AGM

If the AGM is held on 30 April 2026, the Bor.Or.Jor.5 filing is due 14 May 2026 at the latest. It goes through the same DBD e-Filing system as the financial statements.

Legal basis: CCC §1139

3. File the financial statements (Sor.Bor.Chor.3) with DBD — within 1 month of the AGM

If you hold the AGM on the last possible day (30 April), the financial statements must be filed by 31 May 2026.

Where many companies get this wrong: this deadline is not fixed at 31 May — it’s counted as 1 month from the actual AGM date. If you hold the AGM earlier, the DBD deadline moves earlier too. An AGM on 15 April means filing by 15 May, not 31 May.

Legal basis: Accounting Act B.E. 2543, §11

4. File PND.50 with the Revenue Department — 150 days after year-end

Counting 150 days from the year-end date, for the December 2025 close that works out to:

- Paper filing: 30 May 2026 at the latest

- Online filing via the Revenue Department’s e-Filing: up to 7 June 2026 (the RD grants +8 days for online returns)

Legal basis: Revenue Code §68

Who has to file financial statements?

Under Accounting Act B.E. 2543, §§8-11, the juristic persons required to keep accounts and file financial statements are:

- Limited companies and public companies — file within 1 month after AGM approval

- Registered partnerships (ห้างหุ้นส่วนจดทะเบียน / ห้างหุ้นส่วนจำกัด) — file within 5 months of year-end (no AGM required)

- Foreign juristic persons doing business in Thailand (branches, representative offices, regional offices) — file within 5 months of year-end

- Joint ventures under Revenue Code §39 — file within 5 months of year-end

For the 31 December 2025 year-end, entities on the 5-month timeline have until 31 May 2026 to file.

Who must sign the financial statements? — The three indispensable signatures

A set of financial statements filed with DBD requires signatures from three different people, under three different laws:

1. Authorized director

- Legal basis: CCC §§1196, 1199, and the company’s registration affidavit (หนังสือรับรอง)

- Who signs: the director(s) authorized to bind the company as stated on the DBD’s affidavit — could be one director alone, two directors jointly, with or without the company seal, depending on what was registered

- Where: the balance sheet / statement of financial position, and the Sor.Bor.Chor.3 transmittal form

2. Accountant / bookkeeper (ผู้ทำบัญชี)

- Legal basis: Accounting Act B.E. 2543, §§7(6), 19, and DBD announcements

- Qualifications: must be a registered accountant in DBD’s e-Accountant system AND a member of the Federation of Accounting Professions (TFAC) — can be an in-house employee or an outsourced provider, but must hold a registration number

- Important distinction the law draws:

- “Person required to keep accounts” (ผู้มีหน้าที่จัดทำบัญชี) = the entity itself (the company)

- “Accountant” (ผู้ทำบัญชี) = the natural person who actually does the bookkeeping

- Where: the financial statements (in the “Accountant” block, with the registration number), and the Sor.Bor.Chor.3 form

Important update: A DBD announcement dated 29 October 2025 (effective 1 January 2026) changed the qualifications for accountants — new registrants must complete a DBD e-Learning module and pass a 60% assessment; CPD is now ≥12 hours per year including at least 1 hour of professional ethics; and the per-accountant cap shifts from “100 clients per year” to “100 financial statements per year.”

3. Certified Public Accountant (CPA) auditor

- Legal basis: Accounting Act B.E. 2543, §11, and the Accounting Profession Act B.E. 2547

- Qualifications: must be a CPA licensed by TFAC with currently-active status (verify at eservice.tfac.or.th)

- Where: the auditor’s report that accompanies the financial statements (separate from the balance sheet signed by the director and accountant)

- No backdating: the audit report’s signing date must be the date on which the auditor actually completed obtaining sufficient evidence

Exception: small registered partnerships may use a TA instead of a CPA

Under a Ministerial Regulation (B.E. 2544) issued under the Accounting Act, a small registered partnership meeting all of the following thresholds is not required to use a CPA — they may have their accounts audited and certified by a Tax Auditor (TA) licensed by the Revenue Department instead:

- Registered capital ≤ THB 5 million

- Total assets ≤ THB 30 million

- Total revenue ≤ THB 30 million

Note: this exemption applies only to partnerships — every limited company (even with THB 1 million paid-up capital) must use a CPA.

DBD e-Filing is mandatory (since 2017)

DBD no longer accepts paper filings of financial statements, as of 1 January 2017. All filings must go through efiling.dbd.go.th in the DBD’s XBRL-in-Excel format.

Things to watch:

- Companies that have never registered must obtain an e-Filing username/password at least 1 month in advance — the process includes identity verification

- Both the authorized director and the accountant must sign digitally in the system; wet-ink signatures aren’t accepted for e-filings

- No deadline extension for DBD filings (unlike the Revenue Department’s +8 days for online tax returns)

What happens if you miss the deadlines?

DBD (Accounting Act §30): failure to file financial statements on time carries a criminal fine up to THB 50,000 for both the company AND each authorized director, assessed separately. In practice, DBD uses a graduated settlement schedule based on how late the filing is.

Revenue Department (Revenue Code §§35, 27):

- Late PND.50 filing up to 7 days late — THB 1,000 fine

- More than 7 days late — THB 2,000 fine

- 1.5% per month surcharge (เงินเพิ่ม) on any unpaid tax, capped at 100% of the tax

Crucially: under Accounting Act §40, when a juristic person commits an offence under the Act, the directors, managing partner, or person responsible for the operation of the business are deemed to have committed the offence jointly — unless they prove they had no knowledge of or did not consent to the offence. That means directors are personally liable, not just the company.

Plan ahead to manage the risk

For a December 31 year-end, the right rhythm is:

- January – February: close the books, prepare financial statements

- February – March: auditor performs the audit and issues the report

- Early April: schedule the AGM, send meeting invitations (at least 7 days prior)

- Late April: hold the AGM, approve the accounts

- May: file Bor.Or.Jor.5 + financial statements with DBD, and PND.50 with the Revenue Department

The audit must be finished before the AGM — the meeting approves the audited accounts, not a draft.

Need a hand?

Our firm handles the whole cycle — from year-round bookkeeping and year-end close to CPA audit to tax return filings. We’ve kept every one of our clients’ deadlines for more than five years running.

Get in touch for a free initial consultation — the earlier the better, because auditors have limited capacity in peak season.

Note: This article is general guidance for understanding, not case-specific legal advice. For questions about your particular business situation, we recommend speaking with an advisor directly.